FinTech: Open Banking

What is Open Banking?

Open Banking is exactly what it sounds like; it is the opening of internal bank data and processes to be shared with external parties through various channels. What does this mean? In its essence it means that control over all the data collected and held by your primary banks will be given back to you. This data that you will now be in control of may look like:

Product data: Information about rates, fees and features of bank products

Customer data: Personal information about you like your phone number, email address, home address

Account data: Information on specific accounts such as balances, direct debits, regular repayments

Transaction data: Information on your transactions, like how much you spent and where you made the transaction

With this data, you will be able to more readily grant access to third-party financial institutions so that they can provide a whole range of improved products and services to better help you in managing your finances. The introduction to open banking will vastly change the currently monopolised banking industry that revolves around the big 4 banks (ANZ, Commbank, NAB, Westpac) and open up the market to new competitors that will drive innovation and product competition.

How it works?

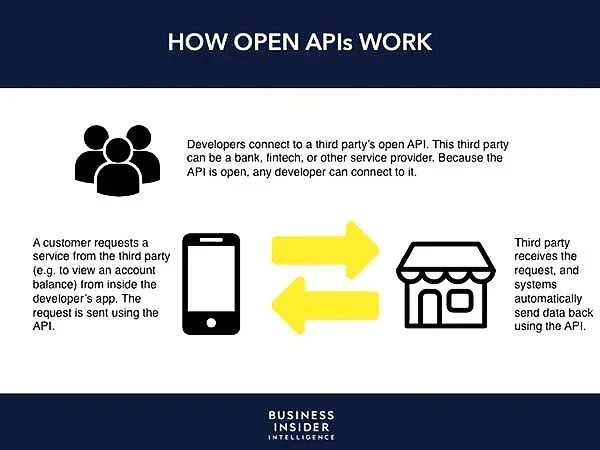

With the implementation of the Open Banking systems, banks will have to open up their application programming interfaces (APIs), allowing third parties to access the financial information which will be used to create new apps and services.

What is an API?

APIs are a set of codes and protocols that determines how different software components should interact, essentially allowing different applications to communicate with each other. For any consumer this is an opt in process, meaning that no information will be shared without their knowledge or consent. With explicit consent, third-party financial providers will be able to utilize this access to the shared banking data through APIs towards creating better services and apps to help manage your finances.

What this means for you?

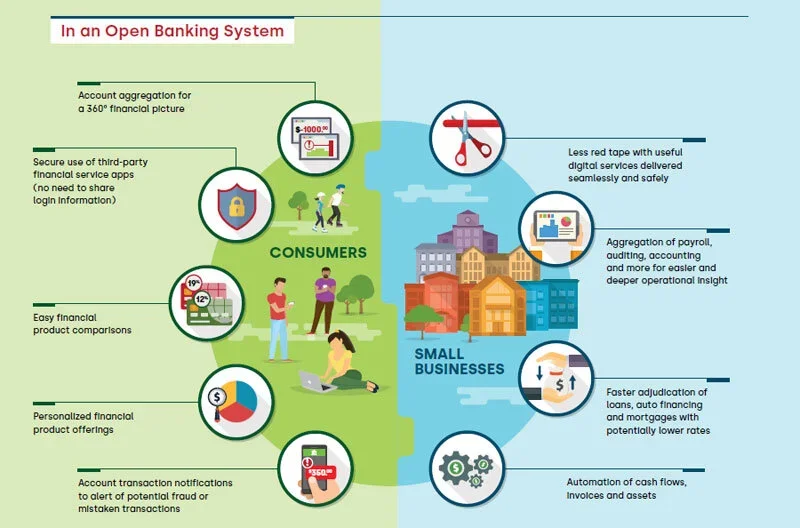

The data will be a collection of all your banking activities, providing insights into how you are spending money, saving or growing debt. This data will hold crucial information as it will essentially form the persona of who you are as a participant in the economy. Currently, for people to get this holistic picture of their finances they had to manually compile their financial information across all the platforms in one place before sending it off to a financial provider. With open banking, this data will be compiled in a universally recognised format for various providers to access. This new ease of access will open up the possibilities for financial institutions to provide a myriad of new products and services such as:

More in-depth analyses into spending and earnings for better future budgeting

Better product recommendations such as improved interest rates

Improving the process and information sharing required when applying for loans

More convenient and better tailored financial services

Better repayment plans

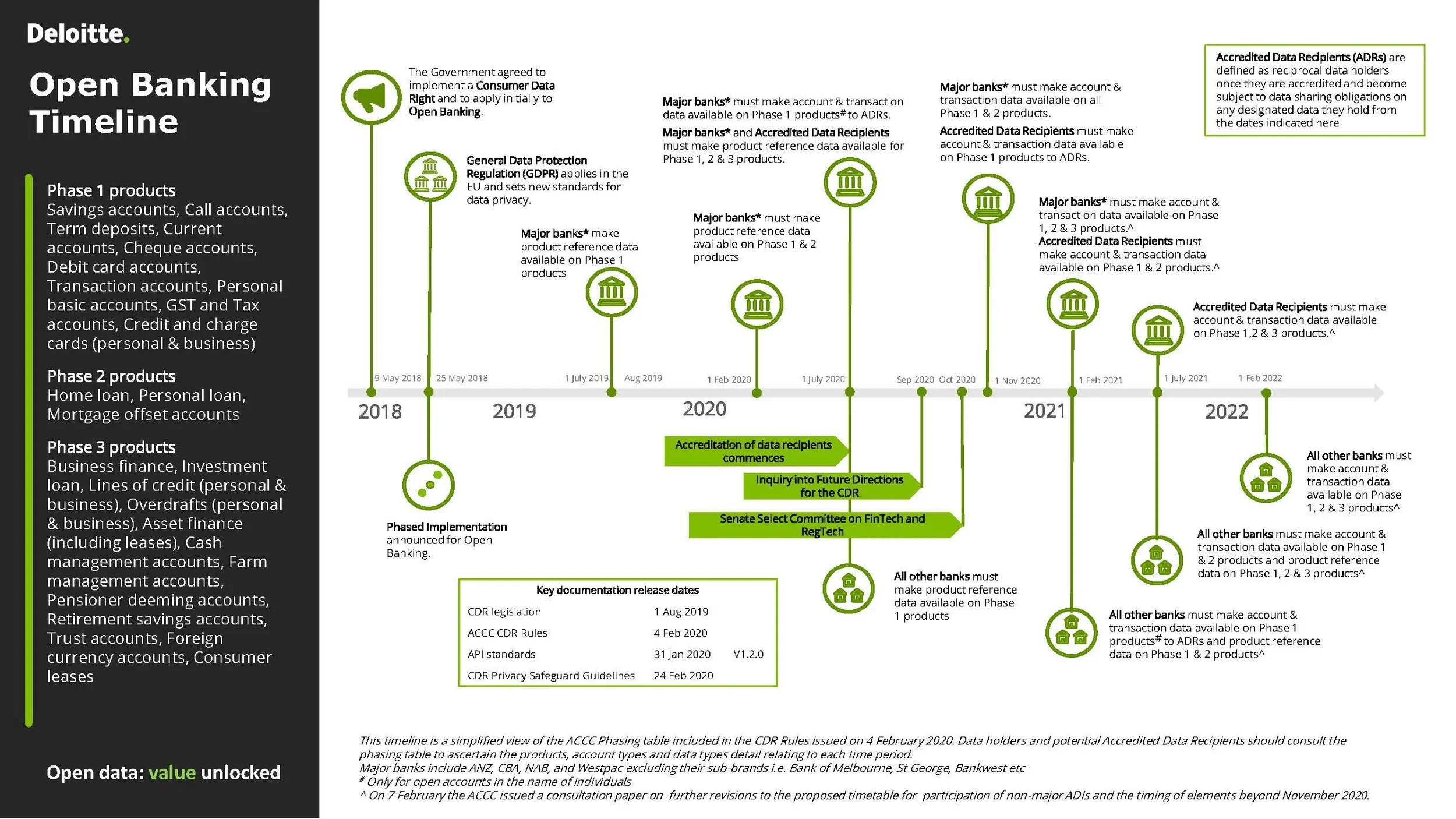

Open-Banking Timeline in Australia

At the beginning of August 2019, Australia began its movement towards an open data economy by passing the Consumer Data Right (CDR) legislation in parliament. This new legislation allowed consumers control over their data, enabling them to share it with third parties. As the rules and regulations surrounding privacy and information security are finalised, the process of accrediting third parties access to these APIs will begin. This will mean that Banks and financial organisations looking to be accredited will have begun preparing for this wave of change to leverage the opportunities that shared data provides.

Will your data be safe?

This move from a closed environment that exists currently within the banking system will bring a level of openness that will undoubtedly increase it’s vulnerability to new threats. Everything from the spoofing of a customer’s consent to intercepting the communications between the user and third-party and commandeering the data will now all become a possibility. Since open banking is based on the use of APIs that enables third parties to build applications and services, attacks on the building blocks of an API that allows one piece of software to communicate with another will undeniably be the biggest security threat.

However, just because the threat of security risks exists does not mean that any innovation towards open data sharing will not be possible. This means that not only incorporating advanced API-management tools but also that ensuring they exist on foundational security layers will be essential. It is crucial that the banks leading the transformation charge into an open sphere of financial data are proceeding with the security and privacy of our financial data at the heart of everything.

This article is published by CCA, a student association affiliated with Monash University. Opinions published are not necessarily those of the publishers. CCA and Monash University do not accept any responsibility for the accuracy of information contained in the publication.